Case Study: Validating Alpha with Synthetic Data

Customer need: A validation framework capable of measuring robustness across hypothetical but plausible scenarios. Traditional backtesting has a fundamental limit: it can only tell us how a strategy would have performed on the single specific sequence of events that happened in the past. This "sample size of one" problem raises a critical question for risk managers: "How do we know this strategy didn't just get lucky?"

The Solution: Sabr Research architected and deployed a Model Based Simulation Framework. This generative module allows the system to move beyond historical playback by generating thousands of plausible market universes. Such an approach allows the client to measure robustness, quantify uncertainty, and build genuine confidence in a strategy's resilience across hypothetical scenarios.

Closing the Trust Gap

In most industries, rigorous simulation is non negotiable. No aircraft is certified to fly without exhaustive stress tests in wind tunnels and digital simulators. No new drug reaches patients without being validated across countless scenarios in clinical trials. Failure in these fields is unacceptable, and simulation is one of the main safeguards engineers use to ensure reliability before a system ever faces the real world.

The financial sector, interestingly, often takes the opposite approach. Despite the fact that failure here may cost fortunes or destabilize markets, robust simulations are rare. The most traditional form of evaluation, backtesting, is frequently treated with suspicion or conducted so poorly that managers fall back on intuition.

This framework bridges that gap. By adopting simulation, we bring the same scientific standards to finance that are taken for granted in aviation, automotive engineering, and pharmaceuticals. It shifts the question from "Did this work in the past?" to "Will this work in the future, even if conditions change?"

However, trust is earned, not assumed. For professionals to rely on synthetic data, the simulation engine must demonstrate specific capabilities. These include the ability to reproduce the statistical signatures of real historical data to prove baseline realism, transparent parametrization so users understand how specific inputs drive market trends, and the ability to trace synthetic events back to their root causes. While not an exhaustive list, these features are essential to turn a black box generator into a verifiable scientific instrument.

Technical Deep Dive: Model Based Scenario Generation

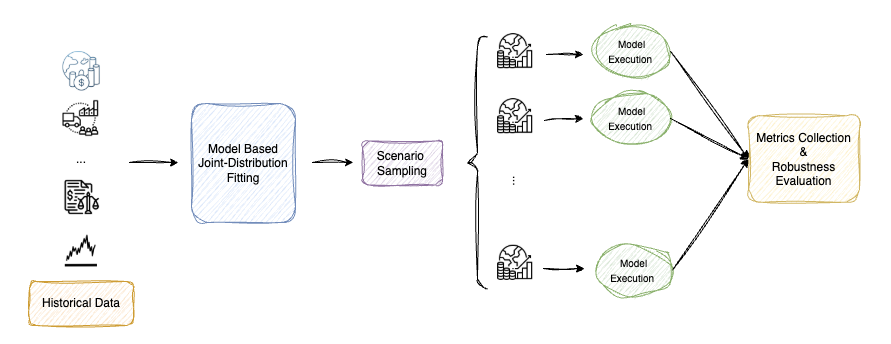

Achieving this required powerful scenario generation tools. Simply reshuffling historical data (bootstrapping) often breaks the temporal structure of markets. Instead, the solution utilizes advanced generative models to learn the joint distribution of key market variables.

Figure 1: The Model Based Simulation Pipeline. Historical data feeds into a joint distribution fitting stage, where relationships among variables are modeled to sample thousands of alternative scenarios.

The system analyzes fundamentals, prices, and volumes across many assets simultaneously, capturing complex dependencies like volatility clustering and heavy tails. Once this mathematical structure is learned, the engine can sample new scenarios from this distribution. These synthetic, yet plausible, scenarios behave like realistic markets without being exact replays of history.

This allows researchers to explore counterfactuals: what if fundamentals evolved differently? What if correlations spiked across sectors earlier than expected?

The result is not a single number but a probabilistic picture of potential outcomes. For example, a model might outperform its benchmark in 70% of simulated worlds, underperform meaningfully in 10%, and fall somewhere in between for the remainder. Strong performance across simulated scenarios not only validates the model's predictive capabilities but also demonstrates that it has learned a robust set of underlying market patterns, rather than simply overfitting to historical noise.

A Philosophical Shift

Ultimately, moving beyond backtesting toward model based scenario generation aligns financial research with the scientific standards of other high stakes industries. Just as aviation and pharmaceuticals rely on rigorous simulations before exposing lives to risk, asset managers can rely on these tools to safeguard capital and improve decision making. This represents more than a methodological upgrade; it is a philosophical one: treating financial systems with the same discipline, humility, and rigor that complex, high stakes systems demand. The Sabr Research platform facilitates this transition, providing the tooling necessary to move from retrospective analysis to forward looking, scientific validation.