Case Study: High Performance Backtesting Infrastructure

Customer need: Research teams were bottlenecked by slow, monolithic simulation engines. A single backtest could take hours, limiting the number of hypotheses a researcher could test in a day.

The Solution: Sabr Research delivered a Distributed Backtesting Cloud, a scalable, serverless framework that allows quant teams to parallelize thousands of simulations. This infrastructure empowers clients to validate investment hypotheses in minutes, not days, without compromising statistical rigor.

Why Clients Upgrade Their Infrastructure

For modern asset managers, backtesting is the primary laboratory. It simulates how a strategy would have performed using historical data to estimate future resilience. However, legacy systems often force a trade off: you can either test fast (using simplified logic) or test accurately (using complex transaction costs and slippage models).

This Distributed Backtesting Cloud eliminates this trade off. By leveraging serverless compute, we allow clients to run high fidelity simulations at scale. This helps Risk Committees answer critical questions before approving capital:

- Does this strategy deliver consistent alpha after full transaction costs?

- Is the logic robust across different volatility regimes (e.g. 2008 vs 2021)?

- How sensitive is the P&L to liquidity constraints?

- Does the signal decay out of sample?

By automating these checks, the platform allows research teams to "fail fast", discarding weak ideas quickly so they can focus on the winners.

Solving the "Crisis of Reproducibility"

A major pain point we solve for Chief Investment Officers (CIOs) is inconsistency. In many firms, Researcher A uses a different backtest engine than Researcher B. This leads to incompatible comparisons that confuse investment committees. The unified platform enforces standardization across the organization, preventing common pitfalls:

Eliminating Overfitting

The engine includes automated "hold out" partitioning, preventing researchers from tuning their models on the test set.

Removing Lookahead Bias

The platform's "Point in Time" data architecture ensures that a simulation running in 2015 only "sees" data available in 2015, preventing the use of future knowledge.

Quantifying Uncertainty

Instead of a single Sharpe ratio, the engine outputs confidence intervals, helping clients understand the statistical significance of their results.

Enforcing Consistency

A unified code base ensures that every researcher in the client's organization computes metrics like "Drawdown" exactly the same way.

This infrastructure transforms backtesting from a "local script" into an enterprise level "truth engine."

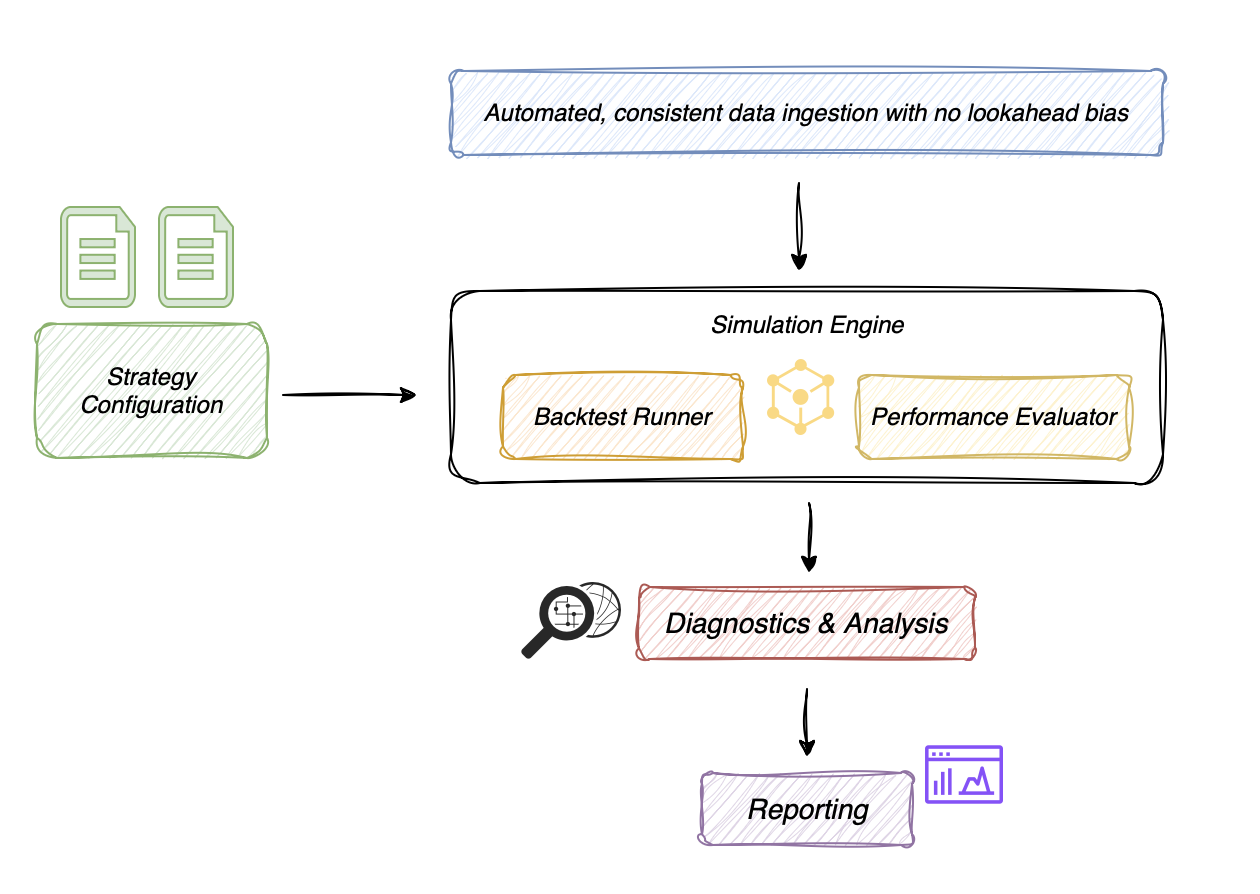

Architecture: Engineering for Scale

Figure 1: The Cloud Architecture delivered to clients.

We designed this framework with one goal: to allow clients to scale their research without scaling their headcount. The architecture rests on modular principles:

Unified Data Interface

A single API for all market data ingestion, ensuring that every simulation starts from the same source of truth.

Centralized Metric Engine

Performance logic (Sharpe, Sortino, Calmar) is decoupled from strategy logic, ensuring 100% mathematical consistency across the firm.

Horizontal Scaling

Simulations are stateless and containerized, allowing the system to spin up 1,000+ parallel workers on demand.

Open API Design

The framework is extensible, allowing client researchers to plug in custom libraries or proprietary alpha models effortlessly.

Beyond core metrics, the platform automatically generates standardized "tear sheets" for every simulation, visualizing sector exposures, regime sensitivity, and signal decay. This gives Portfolio Managers a comprehensive view of a strategy's behavior before a single dollar is deployed.

Accelerating the Alpha Loop

Backtesting is the engine room of any quantitative firm. By upgrading to this Distributed Backtesting Cloud, our clients have successfully closed the gap between research and execution. They have moved from ad hoc scripts to a disciplined, industrial scale pipeline. In a market where speed and rigor are the only advantages that matter, Sabr Research provides the infrastructure that keeps elite teams ahead of the curve.